Today my 6-years old son came with a math homework. The stated goal was to learn the different ways to make 10 out of smaller numbers. I was impressed. Immediately, I wondered

how many ways are there to make 10 out of smaller numbers?

This is one of the beauties of maths: a very simple problem, which a 6-years old can understand, may actually be quite fundamental. If you want to solve this in the general case, for any number instead of 10, you end up with the partition function. And in order to find this, you will probably learn recurrence relations. So what is the answer for 10?

42

Then I looked at one exercise they did in class, which was simply to find different ways to pay 10 euros with bills of 10, 5 and coins of 2 and 1 euro(s).

Many benchmarks show impressive performance gains with the use

of Numba or Pypy. Numba allows to compile just-in-time some specific methods, while Pypy takes

the approach of compiling/optimizing the full python program: you use it just like the standard

python runtime. From those benchmarks, I imagined that those tools would improve my 2D Heston PDE solver

performance easily. The initialization part of my program contains embedded for loops over several 10Ks elements.

To my surprise, numba did not improve anything (and I had to isolate the code, as it would

not work on 2D numpy arrays manipulations that are vectorized). I surmise it does not play well

with scipy sparse matrices.

Pypy did not behave better, the solver became actually slower than with the standard python

interpreter, up to twice as slow, for example, in the case of the main solver loop which only does matrix multiplications and LU solves sparse systems. I did not necessarily expect any performance improvement in this specific loop, since it only consists in a few calls to expensive scipy calculations. But I did not expect a 2x performance drop either.

While I am sure that there are good use cases, especially for numba, I was a bit disappointed

that it likely would require to significantly change my code to have any effect (possibly to not do the initialization with scipy sparse matrices, but then, it is not so clear how). Also, I

find mostbenchmarks dumb. For example, the 2D ODE solver of the latter uses a simple dense 2D numpy array. On real code,

things are not as simple.

Next I should try Julia again out of curiosity. I tried it several years ago in the context of a simple Monte-Carlo simulation and my experiment at the time

was not all that encouraging, but it may be much better at building PDE solvers and not too much work to port my python code. I am curious to see if it ends up being faster, and whether the accessible LU solvers are any good. If Julia delivers, it’s a bit of a shame for python, since it has so many excellent high quality numerical libraries. Also when I look back at my old Monte-Carlo test, I bet it would benefit greatly from numba, somewhat paradoxically, compared to my current experiment.

I just moved my blog to a static website, created with Hugo, I explain the reasons why here.

You can find more about me on my linkedin profile.

In addition you might find the following interesting:

Out of curiosity, I tried quadprog as open-source quadratic programming convex optimizer, as it is looks fast, and the code stays relatively simple. I however stumbled on cases where the algorithm would return NaNs even though my inputs seemed straighforward. Other libraries such as CVXOPT did not have any issues with those inputs.

Searching on the web, I found that I was not the only one to stumble on this kind of issue with quadprog. In particular, in 2014, Benjamen Tyner gave a simple example in R, where solve.QP returns NaNs while the input is very simple: an identity matrix with small perturbations out of the diagonal. Here is a copy of his example:

library(quadprog)

n <-66Lset.seed(6860)

X <-matrix(1e-20, n, n)

diag(X) <-1 Dmat <-crossprod(X)

y <-seq_len(n)

dvec <-crossprod(X, y)

Amat <-diag(n)

bvec <- y +runif(n)

sol <-solve.QP(Dmat, dvec, Amat, bvec, meq = n)

print(sol$solution) # this gives all NaNs

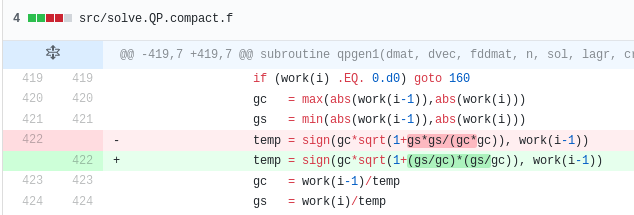

In my specific case, I was able to debug the quadprog algorithm and find the root cause: two variables \(g_c\) and \(g_s\) can become very small, and their square becomes essentially zero, creating a division by zero. If, instead of computing \( \frac{g_s^2}{g_c^2} \) we compute \( \left(\frac{g_s}{g_c}\right)^2 \), then the division by zero is avoided as the two variables are of the same order.

According to the implied cumulative probability density, TSLA has around 15% chance of crashing below $100. Is this really

high compared to other stocks? or is it the interpretation of the data erroneous?

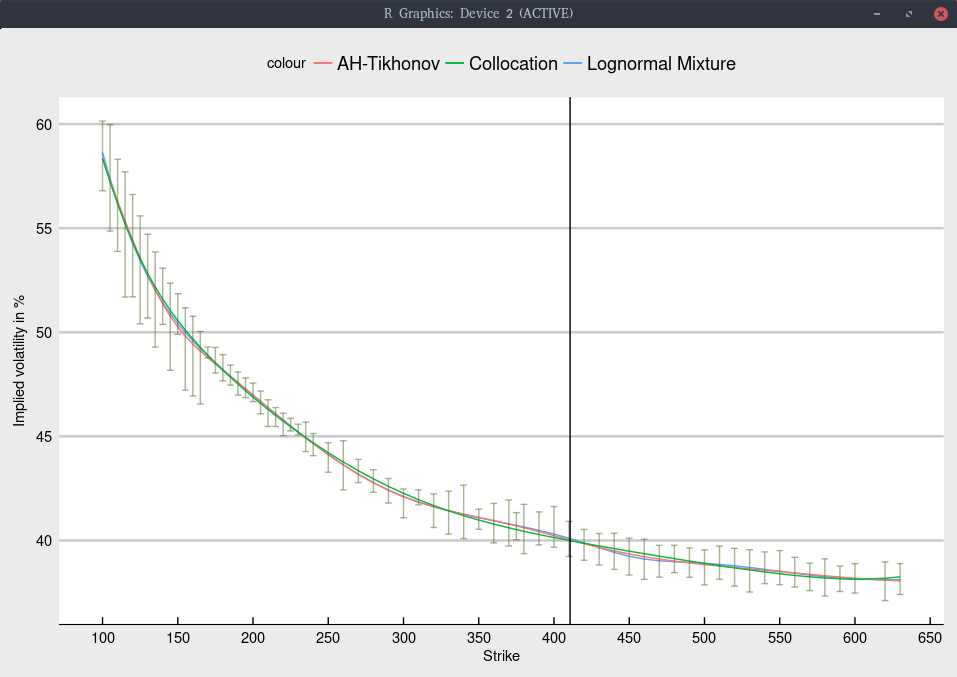

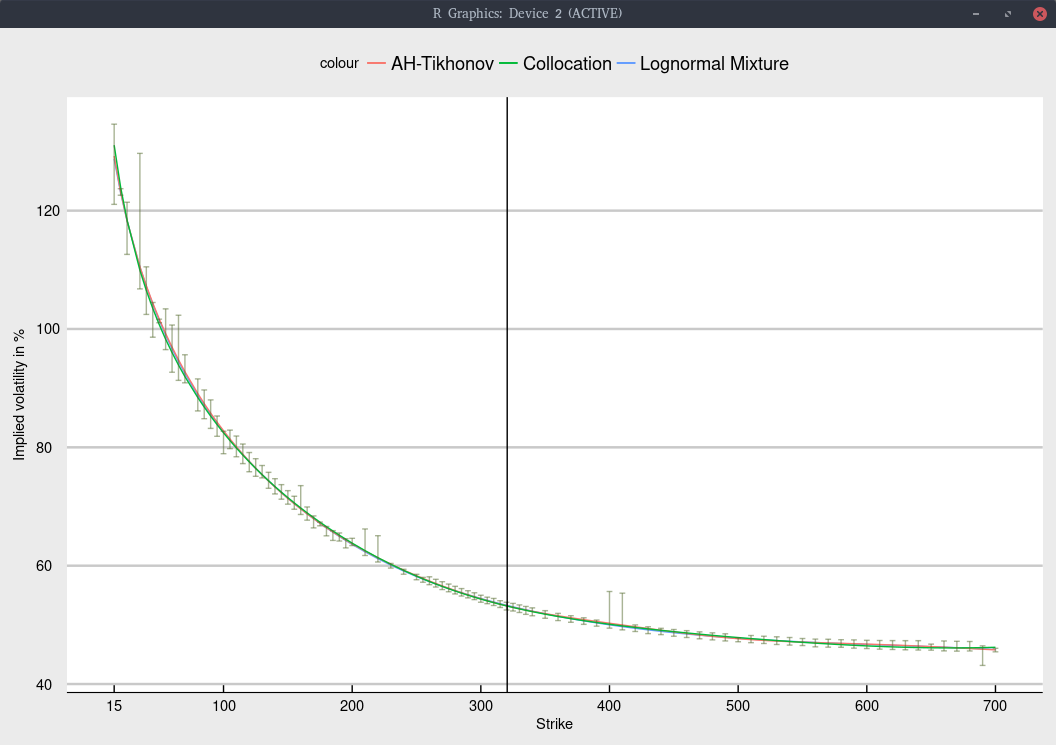

Here I take a look at NFLX (Netflix). Below is the implied volatility according to three different models.

Black volatility implied from Jan 2020 NFLX options.

Again, the shape is not too difficult to fit, and all models give nearly the same fit, within the bid-ask spread as long as we

include an inverse relative bid-ask spread weighting in the calibration.

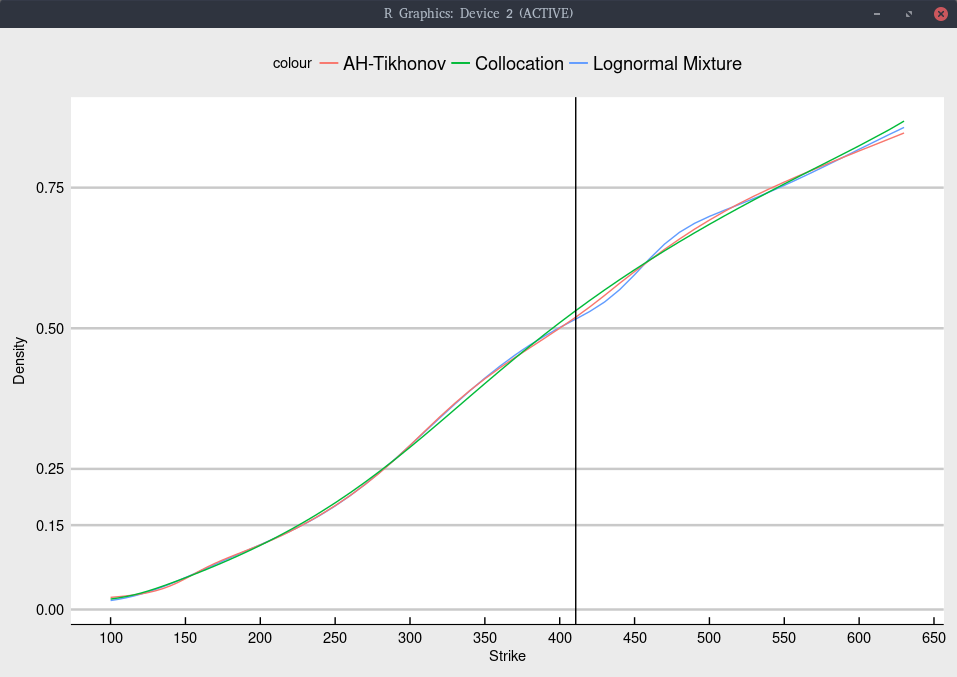

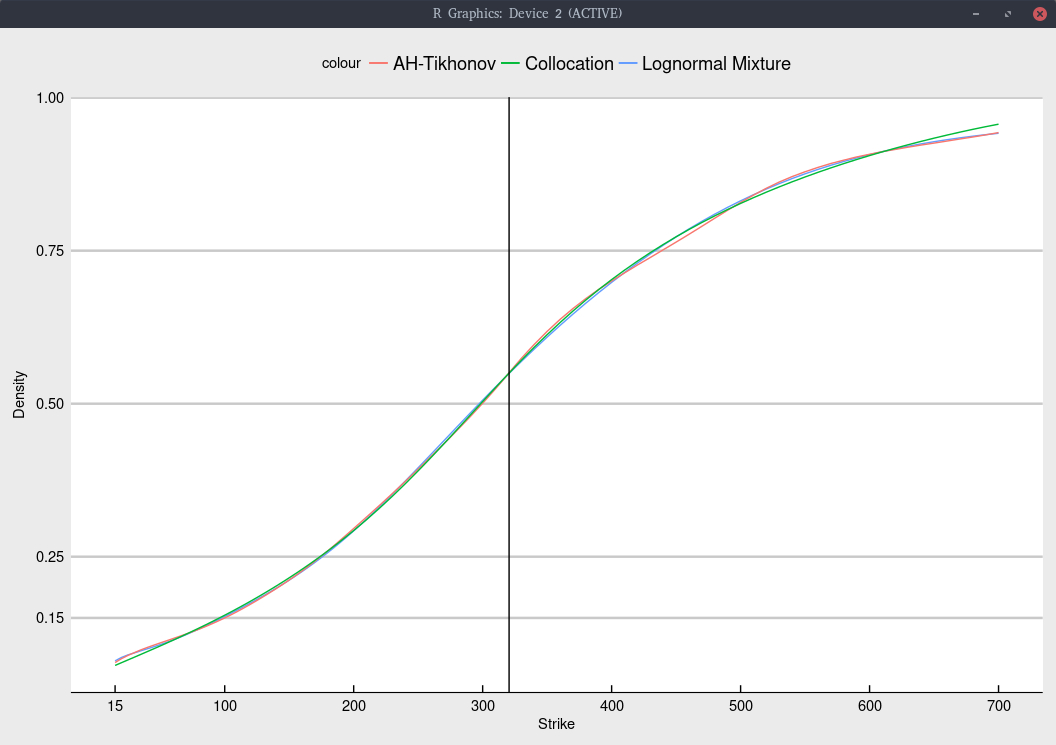

The corresponding implied cumulative density is

Cumulative density implied from Jan 2020 NFLX options.

More explicitely, we obtain

Model

probability of NFLX < 130

Collocation

3.3%

Lognormal Mixture

3.6%

Andreasen-Huge regularized

3.7%

The probability of NFLX moving below $130 is significantly smaller than the probability of TSLA moving below $100 (which is also around the same 1/3 of the spot price).

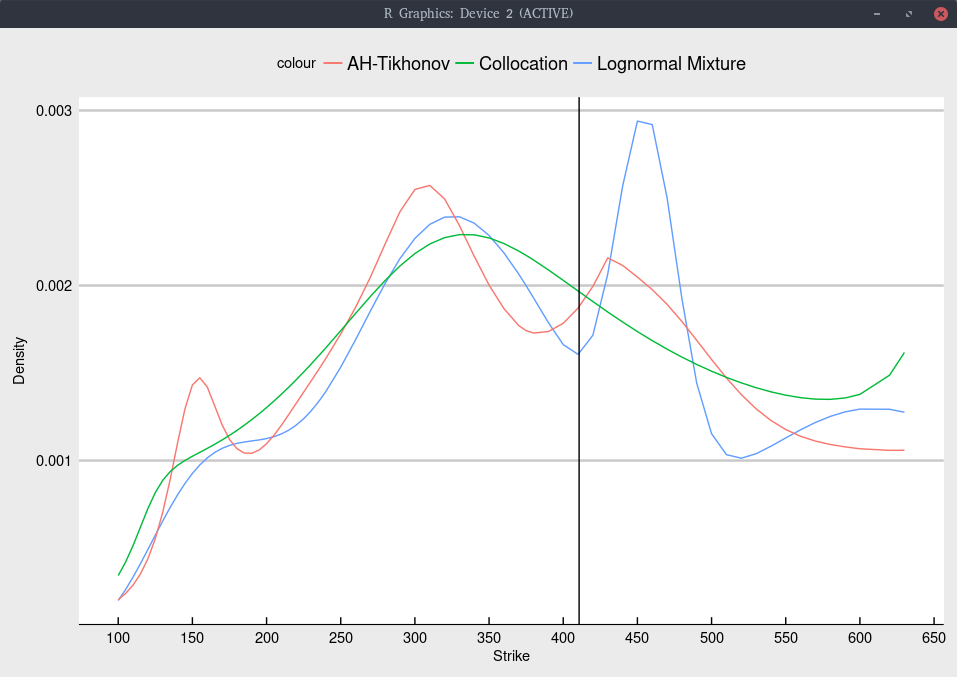

For completeness, the implied probability density is

Probability density implied from Jan 2020 NFLX options.

I did not particularly optimize the regularization constant here. The lognormal mixture can have a tendency to produce

too large bumps in the density at specific strikes, suggesting that it could also benefit of some regularization.

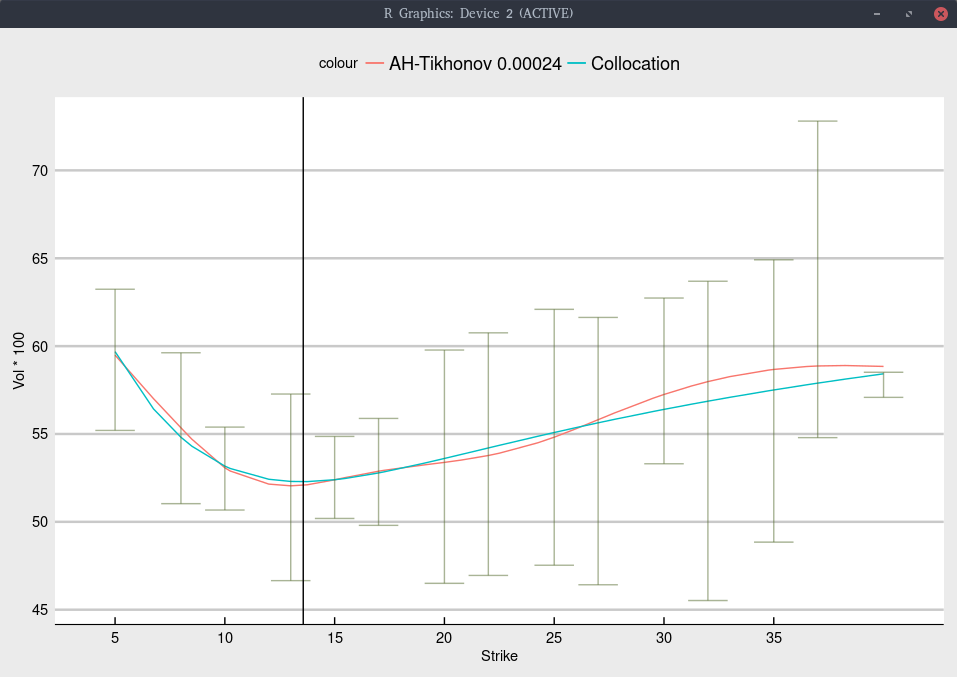

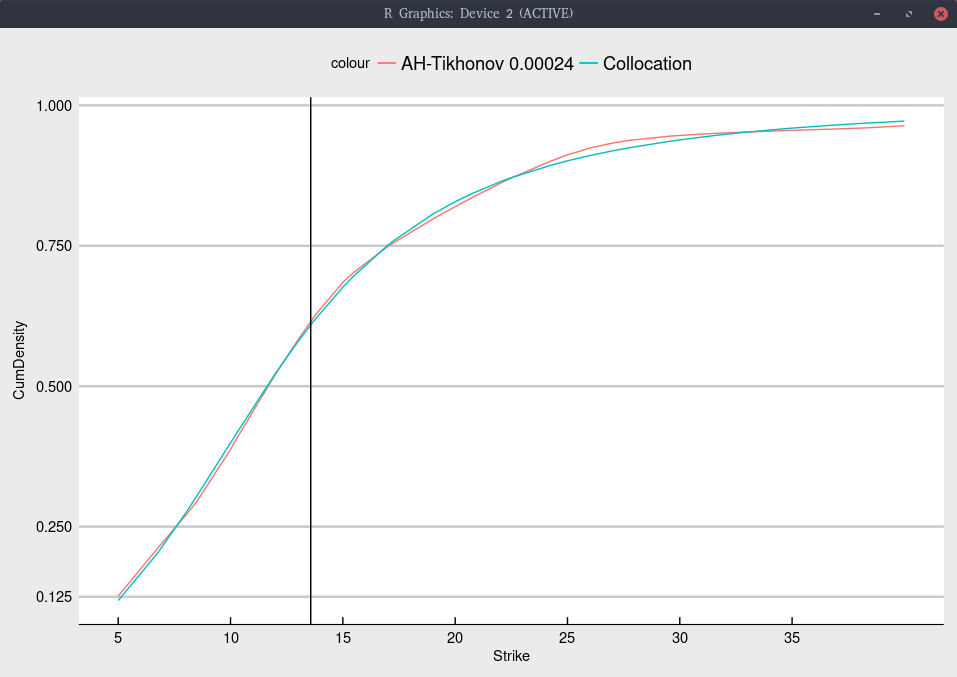

What about risky stocks like SNAP (Snapchat)? It is more challenging to imply the density for SNAP as there are

much fewer traded options on the NASDAQ: less strikes, and a lower volume. Below is an attempt.

Black volatility implied from Jan 2020 SNAP options.

Cumulative density implied from Jan 2020 SNAP options.

We find a probability of moving below 1/3 of the current price lower than with TSLA: around 12% SNAP vs 15% for TSLA.

Timothy Klassen had an interesting post on linkedin recently, with the title “the options market thinks there is a 16% chance that Tesla will not exist in January 2020”.

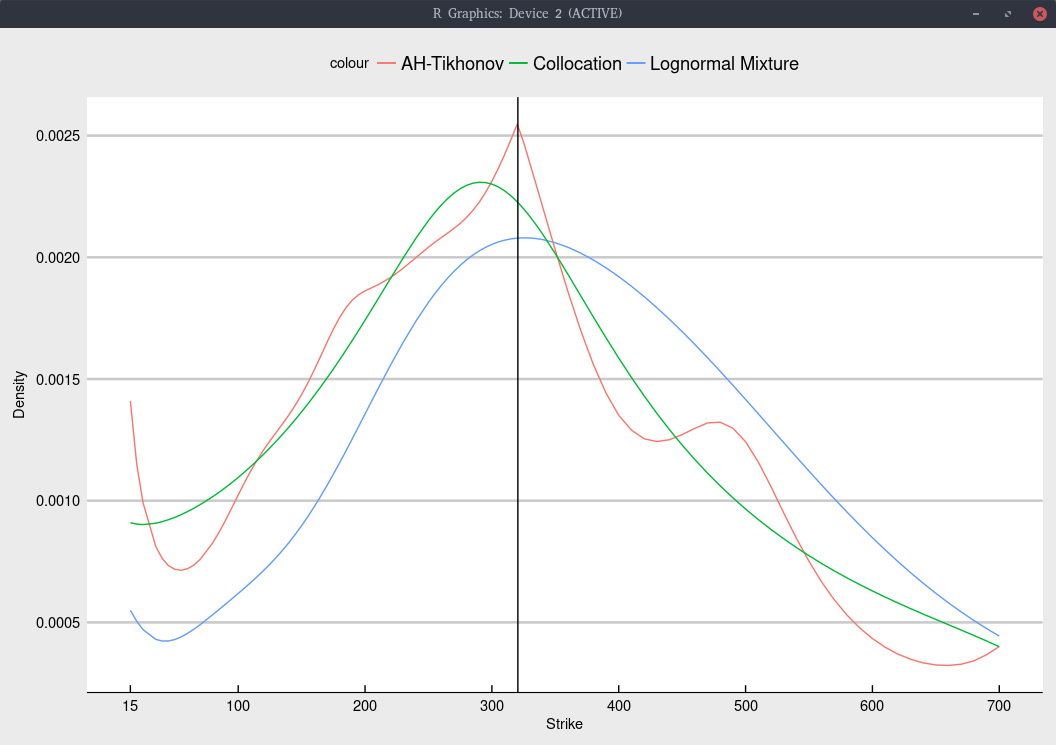

As I was also recently looking at the TSLA options, I was a bit intrigued. I looked at the option chain on July 10th,

and implied the European volatility from the American option prices. I then fit a few of my favorite models: Andreasen-Huge with Tikhonov regularization, the lognormal mixture, and a polynomial collocation of degree 7.

This results in the following graph

Black volatility implied from Jan 2020 TSLA options.

The shape is not too difficult to fit, and all models give nearly the same fit, within the bid-ask spread as long as we

include an inverse relative bid-ask spread weighting in the calibration. Note that I

removed the quote for strike 30, as the bid-ask spread was, unusually extremely large and would only introduce noise.

Like Timothy Klassen, we can look at the implied cumulative density of each model.

Cumulative density implied from Jan 2020 TSLA options.

More explicitely, we obtain

Model

probability of TSLA < 100

probability of TSLA < 15

Collocation

15.4%

7.2%

Lognormal Mixture

15.2%

8.0%

Andreasen-Huge regularized

15.0%

7.7%

It would have been great of Timothy Klassen had shown the implied density as well, in the spirit of my earlier posts on a similar subject.

Probability density implied from Jan 2020 TSLA options.

In particular, the choice of model has a much stronger impact on the implied density. Even though Andreasen-Huge has more

modes, its fit in terms of volatilities is not better than the lognormal mixture model. We could reduce the number of modes by increasing

the constant of the Tikhonov regularization, at the cost of a slightly worse fit.

The collocation produces a significantly simpler shape. This is not necessarily a drawback, since the fit is quite good

and more importantly, it does not have a tendency to overfit (unlike the two other models considered).

Model

weighted root mean square error in vols

Collocation

0.00484

Lognormal Mixture

0.00432

Andreasen-Huge regularized

0.00435

The most interesting from T. Klassen plot, is the comparison with the stock price across time.

It is expected that the probability of going under $100 will be larger when the stock price moves down,

which is what happen around March 27, 2018. But it is not so expected that when it comes back up higher

(above $350 in mid June), the probability of going under $100 stays higher than it was before March 27, 2018,

where the stock price was actually lower.

In fact, there seems to be a signal in his time-serie, where the probability of going under $100 increases

significantly, one week before March 27, that is one week before the actual drop,

suggesting that the drop was priced in the options.

I was wondering if I could use the SABR moments to calibrate a model to SABR parameters directly. It turns out that the SABR moments have relatively

simple expressions when \(\beta=0\), that is, for the normal SABR model (with no absorption). This is for the pure SABR stochatic volatility model, not the Hagan approximation.

For the Hagan approximation, we would need to use the replication by vanilla options to compute the moments.

I first saw a simple derivation of the fourth moment in Xavier Charvet and Yann Ticot 2011 paper

Pricing with a smile: an approach using Normal Inverse Gaussian distributions with a SABR-like parameterisation.

I discovered a more recent (2013) paper from Lorella Fatone et al. The use of statistical tests to calibrate the normal SABR model

with simple formulae for the third and fourth moments (sci-hub.nu is your friend to read this). I had actually derived the third moment myself previously, based on the straighforward approach from Xavier Charvet, which

consists merely in applying the Ito-Doeblin formula several times. Funnily, Xavier Charvet and Yann Ticot make it Irish, by calling it the Ito-Dublin formula.

Now the two papers lead to a different formula for the fourth moment. I did not have the courage to find out where exactly was the mistake of Lorella Fatone et al., as their paper

is much more abstract, and follow a somewhat convoluted path to derive the formula. But I could not find a mistake in Xavier Charvet and Yann Ticot paper. They don’t directly give

the fourth moment, but it is trivial to derive the centered fourth moment from their formulae. By centered, I mean the fourth moment of the process \(F(t)-F(0)\) where \(F(0)\) is the

initial forward price.

$$ \frac{A}{\nu^2}\left(e^{6\nu^2 t}-1\right)+2\frac{B}{\nu^2}\left(e^{3\nu^2 t}-1\right)+6\frac{C}{\nu^2}\left(e^{\nu^2 t}-1\right) $$

with

$$ A = \frac{\alpha^4 (1+ 4\rho^2)}{5 \nu^2},,$$

$$ B = -\frac{2 \rho^2 \alpha^4}{\nu^2},,$$

$$ C = - A - B ,.$$

Fatone et al. includes a factor \(\frac{1}{3}\) in front of \(\rho^2\), which I believe is a mistake. There is however

no error in their third moment.

Unfortunately, my quick mapping idea does not appear to work so well for long maturities.

The Gaussian kernel (as well as to some extent the smoothing spline) let us believe that there are multiple modes in the distribution (multiple peaks in the density). In reality,

Gaussian kernel approaches will, by construction, tend to exhibit such modes. It is not so obvious to know if those are real or artificial. There are other ways to apply the Gaussian kernel,

for example by optimizing the nodes locations and the standard deviation of each Gaussian. The resulting density with those is very similar looking.

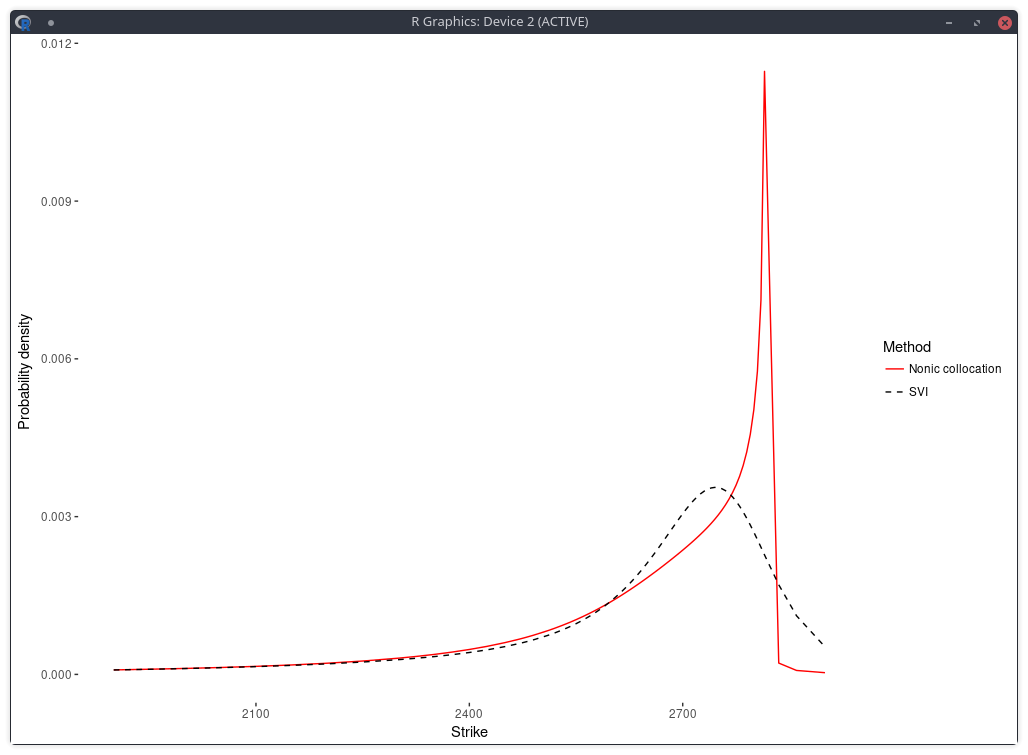

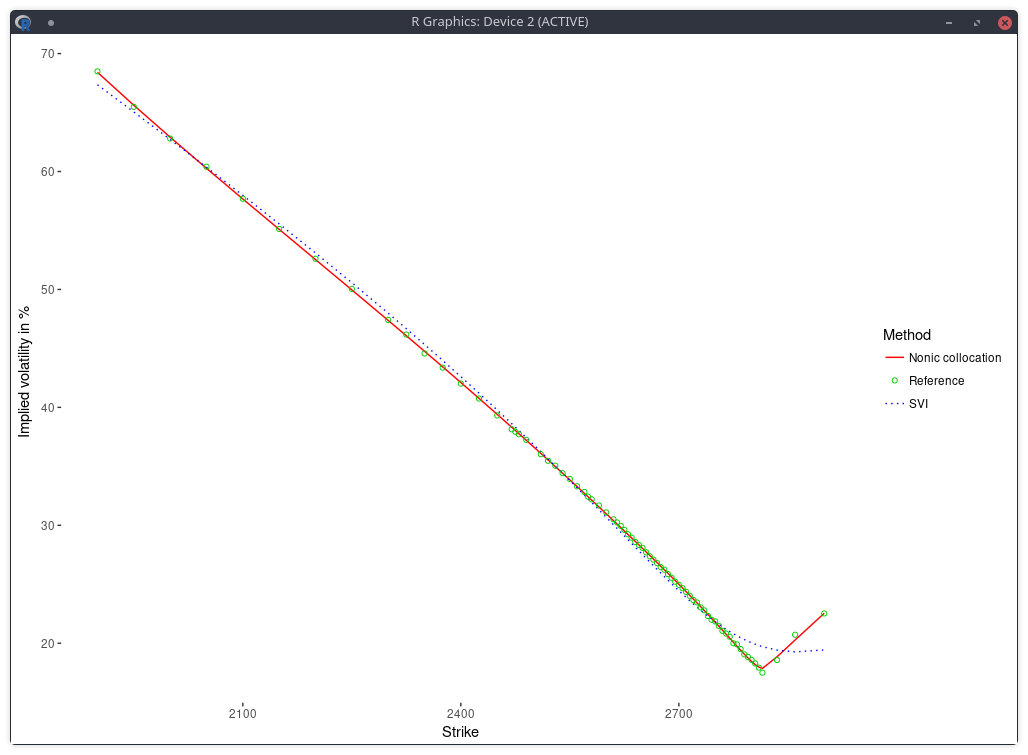

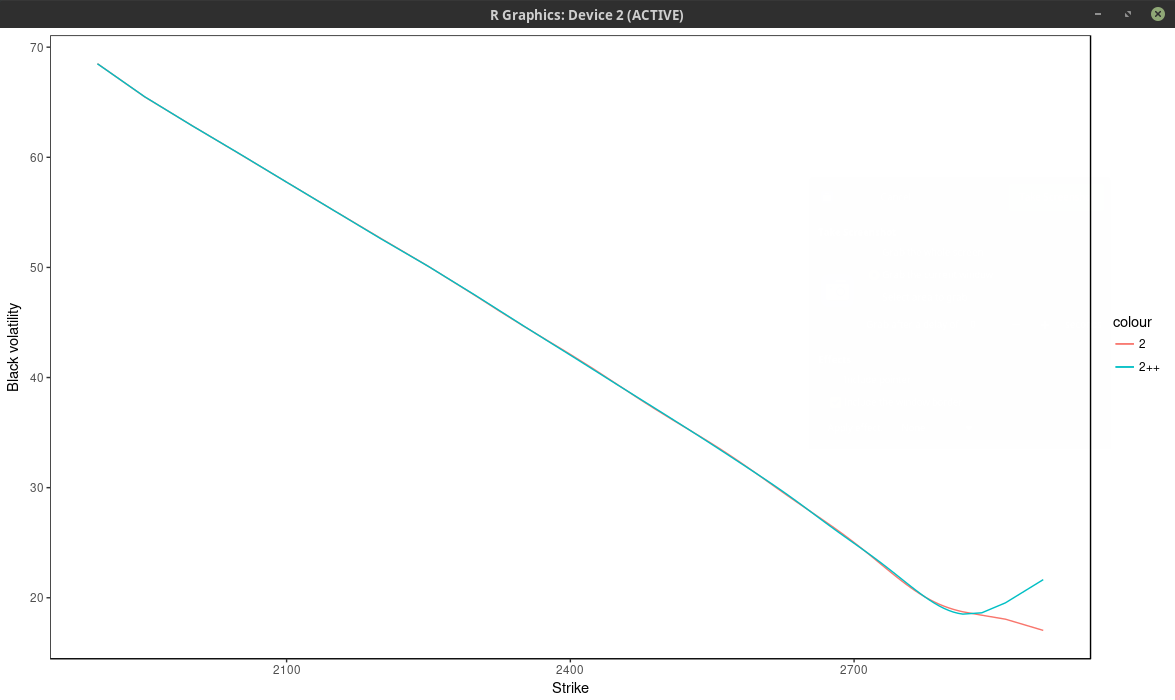

Following is the risk neutral density implied by nonic polynomial collocation out of the same quotes (Kees and I were looking at robust ways to apply the stochastic collocation):

probability density of the SPX implied from 1-month SPW options with stochastic collocation on a nonic polynomial.

There is now just one mode, and the fit in implied volatilities is much better.

implied volatility of the SPX implied from 1-month SPW options with stochastic collocation on a nonic polynomial.

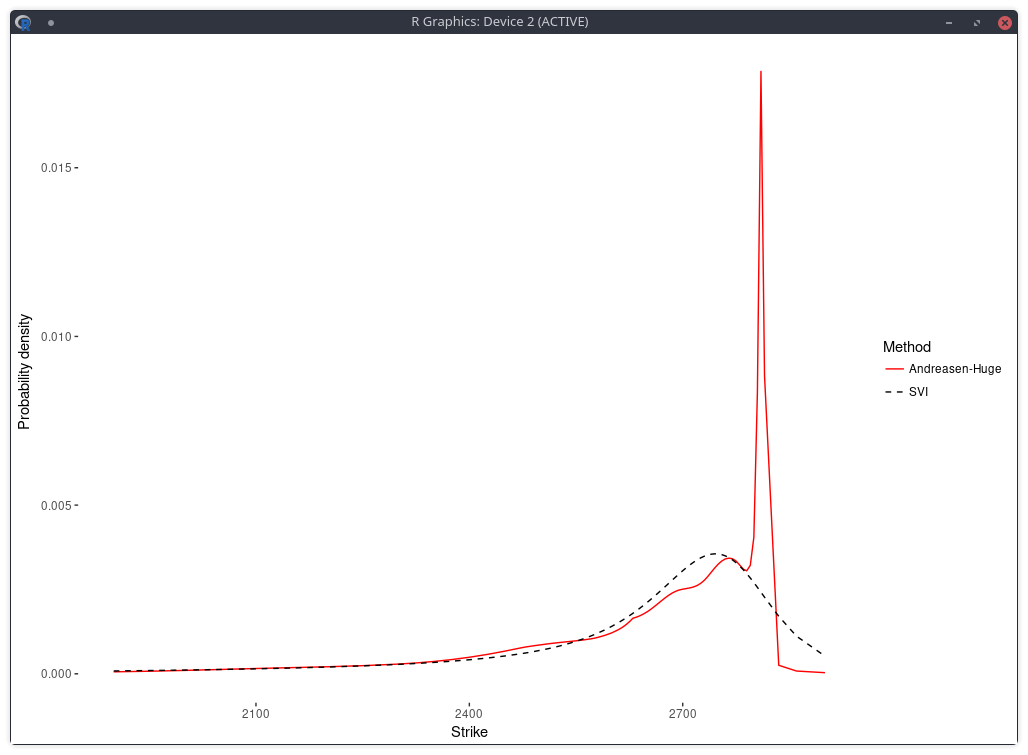

In a related experiment, Jherek Healy showed

that the Andreasen-Huge arbitrage-free single-step interpolation will lead to a noisy RND.

Sebastian Schlenkrich uses a simple regularization to calibrate his own piecewise-linear local volatility approximation

(a Lamperti-transform based approximation instead of the single step PDE approach of Andreasen-Huge).

His Tikhonov regularization consists here in applying a roughness penalty consisting

in the sum of squares of the consecutive local volatility slope differences. This is nearly the same as using the matrix of discrete second derivatives as Tikhonov matrix. The same idea can be found in cubic spline smoothing.

This roughness penalty can be added in the calibration of the Andreasen-Huge piecewise-linear discrete local volatilities and we obtain then a smooth RND:

density of the SPX implied from 1-month SPW options with Andreasen-Huge and Tikhonov regularization.

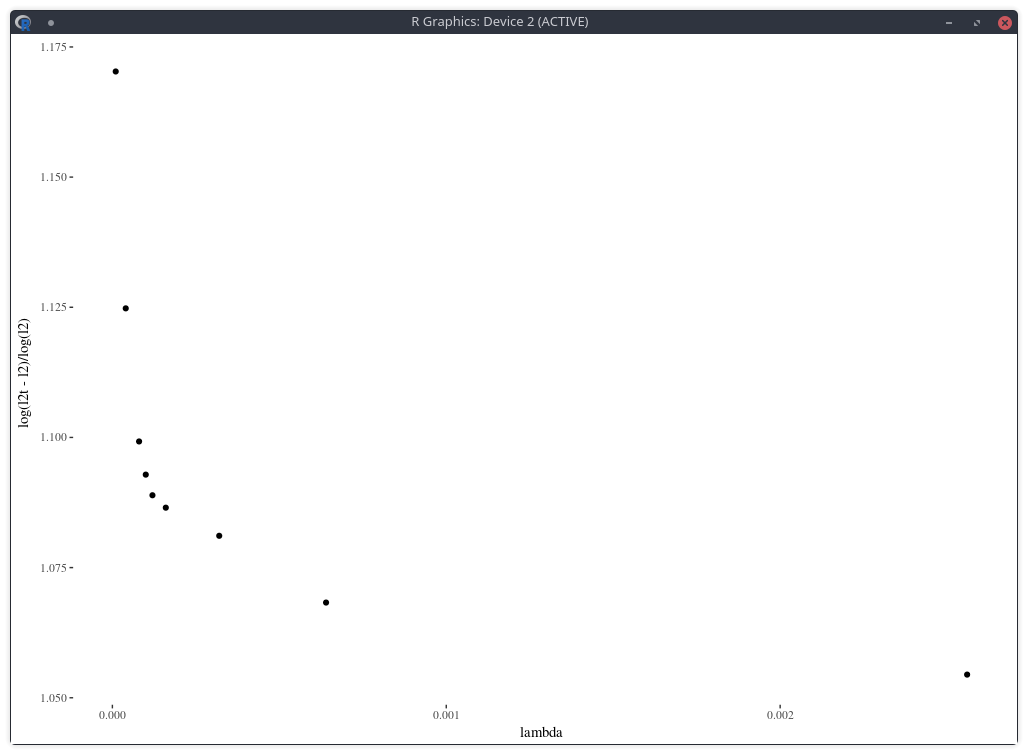

One difficulty however is to find the appropriate penalty factor \( \lambda \). On this example, the optimal penalty factor can be guessed from the L-curve which consists in plotting

the L2 norm of the objective against the L2 norm of the penalty term (without the factor lambda) in log-log scale, see for example this document. Below I plot a closely related function: the log of the penalty (with the lambda factor) divided by the log of the objective, against lambda. The point of highest curvature corresponds to the optimal penalty factor.

density of the SPX implied from 1-month SPW options with nodes located at every 2 market strike.

Note that in practice, this requires multiple calibrations the model with different values of the penalty factor, which can be slow.

Furthermore, from a risk perspective, it will also be challenging to deal with changes in the penalty factor.

The error of model versus market implied volatilies is similar to the nonic collocation (not better) even though the shape is less smooth and, a priori, less constrained as,

on this example, the Andreasen-Huge method has 75 free-parameters while the nonic collocation has 9.

It has been a while since the good old object-oriented (OO) programming is not trendy anymore. Functional programming or more dynamic programming (Python-based) have been the trend, with an excursion in template based programming for C++ guys. Those are not strict categories: Python can be used in a very OO way, but it’s not how it is marketed or considered by the community.

Recently, I have seen some of the ugliest refactoring in my life as a programmer, done by someone with at least 10 years of experience programming in Java. It is a good illustration because the piece of code is particularly simple (although I won’t bother with implementation details). The original code was a simple boolean method on an object such as

This is really breaking OO and moving back to procedural programming.

In a big (but not that big in reality) company, it is quite a challenge to avoid such code transformations. The code might be written by a team with a different manager, managers try to play nice to each other. And is it really worth fighting over such a trivial thing? if some low level (in the company hierarchy) programmer reports this, he is more likely to be labeled as a black sheep. Most managers prefer white sheeps.

More generally software is like entropy: it can start from a simple and clean state, but eventually it will always grow complex and somewhat ugly. And you end up with the Cobol syndrome, where people don’t really know anymore what the software is doing, can’t replace it as it is used (but nobody can tell exactly which parts), and “developers” do only small fixes and evolutions (patches) in an obsolete language on a system they don’t really understand.

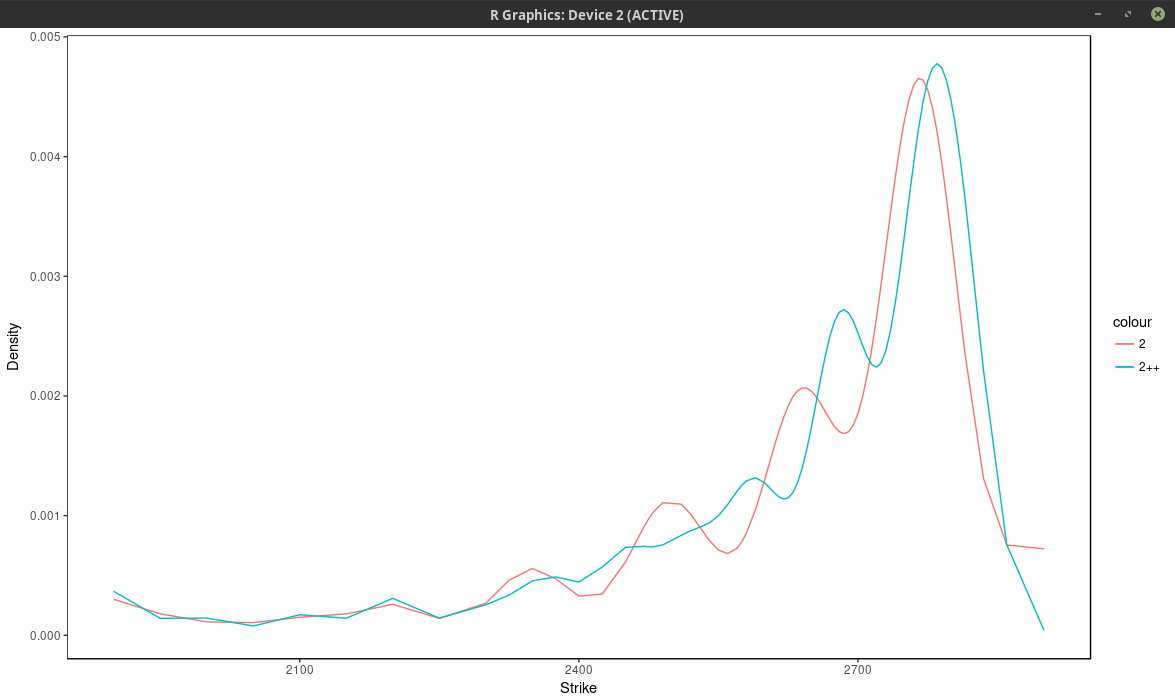

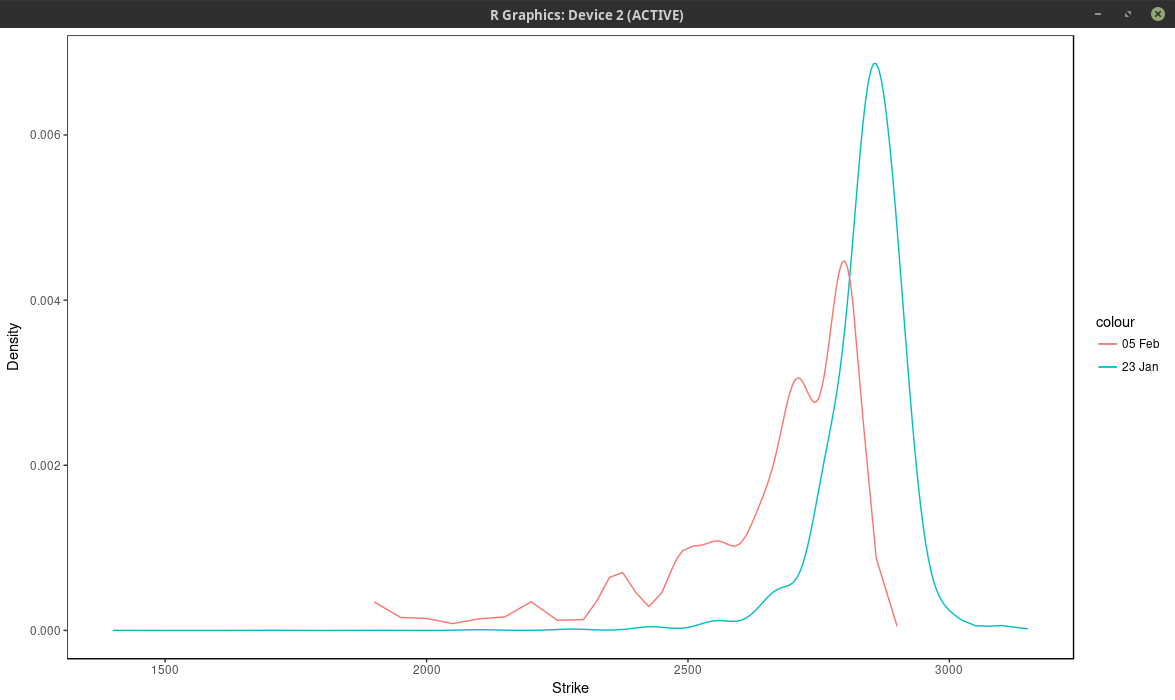

In the previous post, I showed a plot of the probability implied from SPW options before and after the big volatility change of last week.

I created it from a least squares spline fit of the market mid implied volatilities (weighted by the inverse of the bid-ask spread). While it looks reasonable, the underlying

technique is not very robust. It is particularly sensitive to the number of options strikes used as spline nodes.

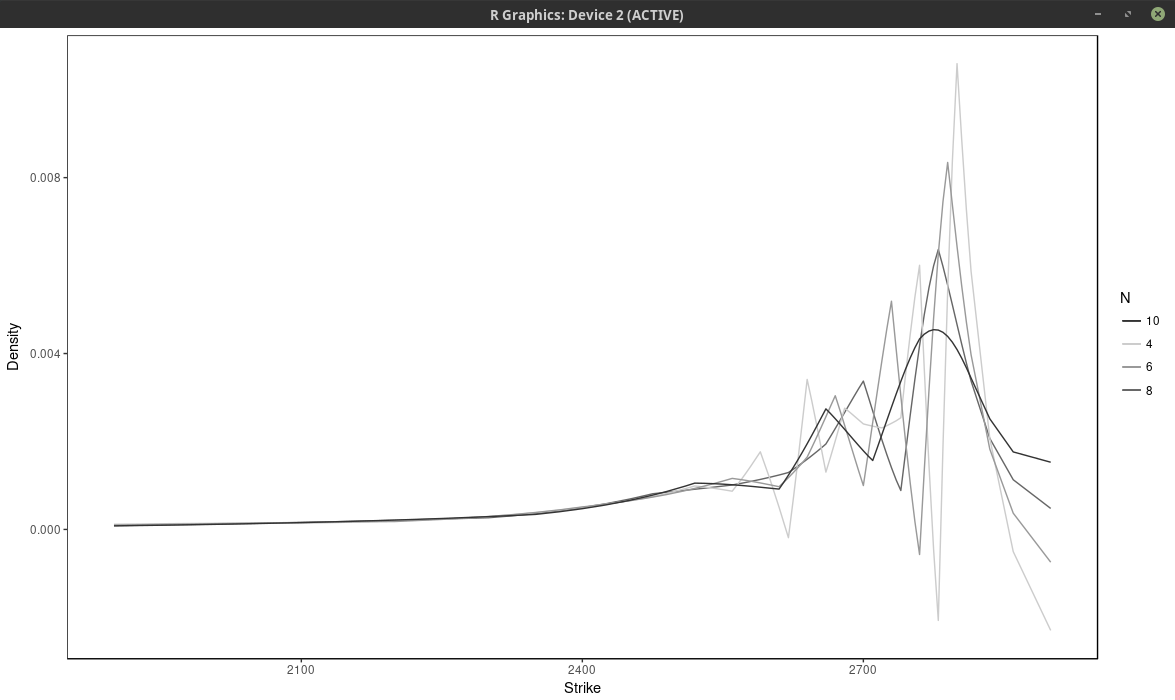

Below I vary the number of nodes, by considering nodes at every N market strikes, for different values of N.

probability density of the SPX implied from 1-month SPW options with nodes located at every N market strike, for different values of N. Least squares spline approach

With \(N \leq 6\), the density has large wiggles, that go into the negative half-plane. As expected, a large N produces a flatter and smoother density. It is not

obvious which value of N is the most appropriate.

Another technique is to fit directly a weighted sum of Gaussian densities, of fixed standard deviation, where the weights are calibrated to the market option prices. This is

described in various papers and books from Wystup such as this one. He calls it the kernel slice approach.

If we impose that the weights are positive and sum to one, the resulting model density will integrate to one and be positive.

It turns out that the price of a Vanilla option under this model is just the sum of vanilla options prices under the Bachelier model with shifted forwards (each “optionlet”

forward corresponds to a peak on the market strike axis). So it is easy and fast to compute. But more importantly, the problem of finding the weights is linear. In deed, the typical

measure to minimize is:

$$ \sum_{i=0}^{n} w_i^2 \left( C_i^M -\sum_{j=1}^m Q_j C_j^B(K_i) \right)^2 $$

where \( w_i \) is a market weight related to the bid-ask spread, \( C_i^M \) is the market option price with strike \( K_i \), \( C_j^B(K_i) \) is the j-th Bachelier

optionlet price with strike \( K_i \) and \( Q_j \) is the optionlet weight we want to optimize.

The minimum is located where the gradient is zero.

$$ \sum_{i=0}^{n} 2 w_i^2 C_k^B(K_i) \left( C_i^M -\sum_{j=1}^m Q_j C_j^B(K_i) \right) = 0 \text{ for } k=1,…,m $$

It is a linear and can be rewritten in term of matrices as \(A Q = B\) but we have the additional constraints

$$ Q_j \geq 0 $$

$$ \sum_j Q_j = 1 $$

The last constraint can be easily added with a Lagrange multiplier (or manually by elimination). The positivity constraint requires more work. As the problem is convex,

the solution must lie either inside or on a boundary. So we need to explore each case where \(Q_k = 0\) for one or several k in 1,…m.

In total we have \(2^{m-1}-1\) subsets to explore.

How to list all the subsets of \( \{1,…,m\} \)? It turns out it is very easy by using a bijection of each subset with the binary representation of \( {0,…,2^m} \). We then just need

to increment a counter for 1 to \( 2^m \) and transform the binary representation to our original set elements. Each element of the subset corresponds to a 1 in the binary representation.

Now this works well if m is not too large as we need to solve \(2^{m-1}-1\) linear systems.

I actually found amazing, it took only a few minutes for m as high as 26 without any particular optimization. For m larger we need to be more clever.

One possibility is to solve the unconstrained problem, and put all the negative quantities to 0 in the result, then solve again this new problem on those boundaries and repeat

until we find a solution. This simple algorithm works often well, but not always. There exists specialized algorithms that are much better and nearly as fast.

Unfortunately I was too lazy to code them. So I improvised on the Simplex. The problem can be transformed into something solvable by the Simplex algorithm.

We maximize the function \( -\sum_j Z_j \) with the constraints

$$ A Q - I Z = B $$

$$ Q_j \geq 0 $$

$$ Z_j \geq 0 $$

where I is the identity matrix. The additonal Z variables are slack variables, just here to help transform the problem. This is a trick I found on a researchgate forum. The two problems

are not fully equivalent, but they are close enough that the Simplex solution is quite good.

With the spline, we minimize directly bid-ask weighted volatilities. With the kernel slice approach, the problem is linear only terms of call prices. We could use a non-linear solver

with a good initial guess. Instead, I prefer to transform the weights so that the optimal solution on weighted prices is similar to the optimal solution on weighted volatilities.

For this, we can just compare the gradients of the two problems:

$$ \sum_{i=0}^{n} 2 {w}_i^2 \frac{\partial C}{\partial \xi}(\xi, K_i) \left( C_i^M - C(\xi, K_i) \right) $$

with

$$ \sum_{i=0}^{n} 2 {w^\sigma_i}^2\frac{\partial \sigma}{\partial \xi}(\xi, K_i) \left( \sigma_i^M - \sigma(\xi, K_i)\right) $$

As we know that

$$ \frac{\partial C}{\partial \xi} = \frac{\partial \sigma}{\partial \xi} \frac{\partial C}{\partial \sigma} $$

we approximate \( \frac{\partial C}{\partial \sigma} \) by the market Black-Scholes Vega and

\( \left( C_i^M - C(\xi, K_i) \right) \) by \( \frac{\partial C}{\partial \xi} (\xi_{opt}-\xi) \),

\( \left( \sigma_i^M - \sigma(\xi, K_i) \right) \) by \( \frac{\partial \sigma}{\partial \xi} (\xi_{opt}-\xi) \)

to obtain

$$ {w}_i \approx \frac{1}{ \frac{\partial C_i^M}{\partial \sigma_i^M} } {w^\sigma_i} $$

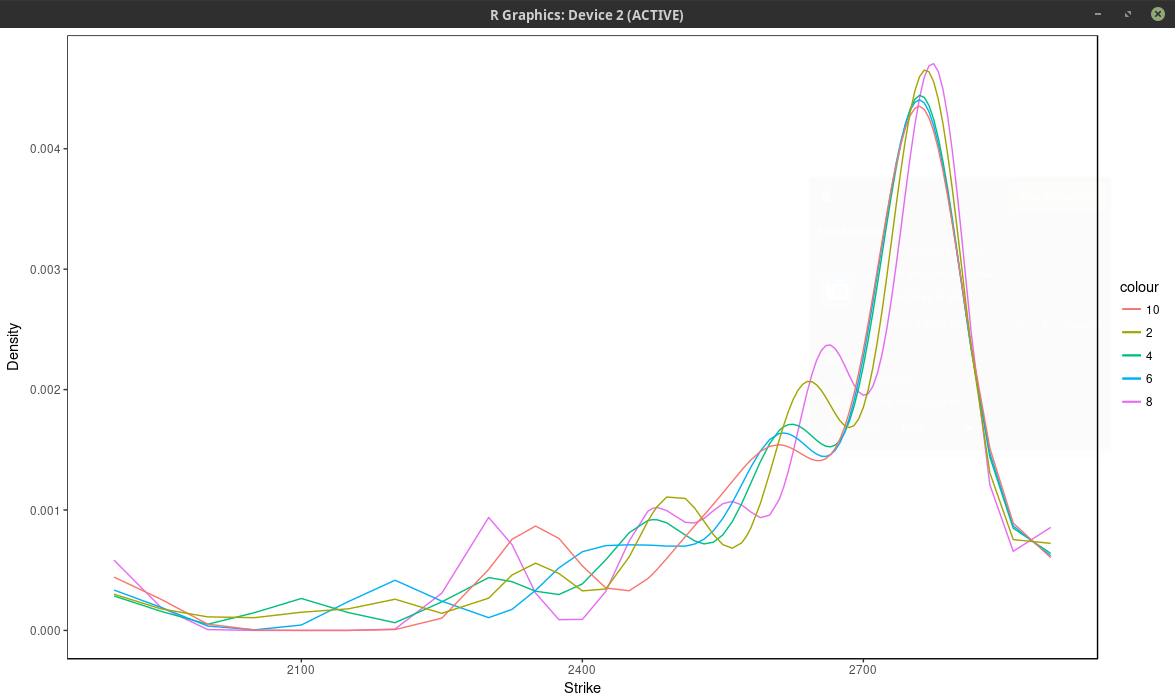

Now it turns out that the kernel slice approach is quite sensitive to the choice of nodes (strikes), but not as much as to the choice of number of nodes. Below is

the same plot as with the spline approach, that is we choose every N market strike as node. For N=4, the density is composed of the sum of m/4 Gaussian densities. We

optimized the kernel bandwidth (here the standard deviation of each Gaussian density), and found that it was relatively insensitive to the number of nodes,

in our case around 33.0 (in general it is expected to be about three times the order the distance between two consecutive strikes, which is 5 to 10 in our case), a smaller value will translate to

narrower peaks.

probability density of the SPX implied from 1-month SPW options with nodes located at every N market strike, for different values of N. Kernel slice approach.

Even if we consider here more than 37 nodes (m=75 market strikes), the optimal solution actually use only 13 nodes, as all the other nodes have a calibrated weight of 0.

The fit can be much better by adding nodes at

f * 0.5, f * 0.8, f * 0.85, f * 0.9, f * 0.95, f * 0.98, f, f * 1.02, f * 1.05, f * 1.1, f * 1.2, f * 1.5, where f is the forward price, even though the optimal solution

will only use 13 nodes again. We can see this by looking at the implied volatility.

implied volatility of the SPX implied from 1-month SPW options with nodes located at every 2 market strike.

Using only the market nodes does not allow to capture right wing of the smile. The density is quite different between the two.

density of the SPX implied from 1-month SPW options with nodes located at every 2 market strike.

I found (surprisingly) that even those specific nodes by themselves (without any market strike) work better than using all market strikes (without those nodes), but

then we impose where the peaks will be located eventually.

It is interesting to compare the graph with the one before the volatility jump:

density of the SPX implied from 1-month SPW options with nodes located at every 2 market strike.

So in calm markets, the density is much smoother and has really only one main mode/peak.

It is possible to use other kernels than the Gaussian kernel. The problem to solve would be exactly the same. It is not clear what would be the advantages

of another kernel, except, possibly, speed to solve the linear system in O(n) operations for a compact kernel spanning at most 3 nodes (which would translate to a tridiagonal system).