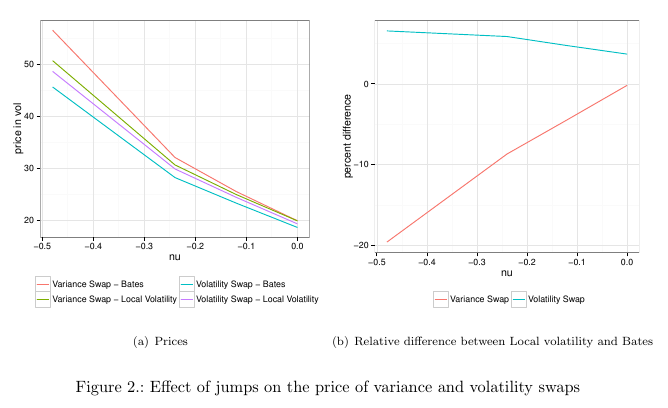

Beside the problem with the discreteness of the replication, variance swaps are sensitive to jumps. This is an often mentioned reason for the collapse of the single name variance swap market in 2008 as jumps are more likely on single name equities.

Those graphs are the result of Monte-Carlo simulations with various jump sizes using the Bates model, and using Local Volatility implied from the Bates vanilla prices. The local volatility price will be the same price as per static replication for the variance swap, and we can see it they converge when there is no jump.

The presence of jumps lead to a theoretically higher variance swap price, again, which we miss completely with the static replication. As jumps go higher, the difference is more pronounced.

Volatility swaps are a bit better behaved in this regard. Interestingly, local volatility overestimate the value in this case (which for variance swaps it underestimates the value). I also noticed that the relatively recent formula from Carr-Lee will underestimate jumps even more so than local volatility: it is more precise in the absence of jumps, very close to Heston, but less precise than local volatility when jumps increase in size.

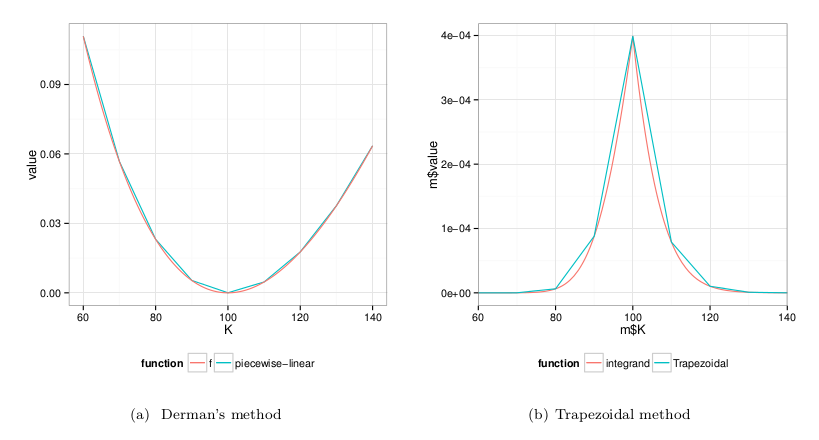

People regularly believe that Variance swaps need to be priced by discrete replication, because the market trades only a discrete set of options.

In reality, a discrete replication will misrepresent the tail, and can be quite arbitrary. It looks like the discrete replication as described in Derman Goldman Sachs paper is in everybody's mind, probably because it's easy to grasp. Strangely, it looks like most forget the section "Practical problems with replication" on p27 of his paper, where you can understand that discrete replication is not all that practical.

Reflecting on all of this, I noticed it was possible to create more accurate discrete replications easily, and that those can have vastly different hedging weights. It is a much better idea to just replicate the log payoff continuously with a decent model for interpolation and extrapolation and imply the hedge from the greeks.

It’s quite incredible that Gnome 3.0 was almost an identical mess as KDE 4.0 had been a year or two earlier. Both are much better now, more stable, but both also still have their issues, and don’t feel like a real improvement over Gnome 2.0 or KDE 3.5.

Now the main file manager for Gnome 3.0, Nautilus has buttons with nearly identical icons that mean vastly different things, one is a menu, the other is a list view. Also it does not integrate with other desktops well from a look and feel perpective, here is a screenshot under XFCE (KDE would not look better).The push for window buttons inside the toolbar makes for a funny looking window. In Gnome Shell, it’s not much better, plus there are some windows with a dark theme and some with a standard theme all mixed together.

On the left is Caja: an updated GTK 2.0 version of Nautilus. I find it more functional, I don’t really understand the push to remove most options from the screen in Gnome 3.0. The only positive thing I can see on for the new Nautilus, is the grey color for the left side, which looks more readable and polished.

Interestingly, Nautilus within Ubuntu Unity feels better, it has a real menu and standard looking window. I suppose they customized it quite a bit.

When it comes to HiDPI support, Gnome shell is often touted has having one of the best. Well maybe for laptop screens, but certainly not for larger screens, where it just double everything and everything just looks too big. XFCE is actually decent on HiDPI screens.

In most financial Monte-Carlo simulations, there is the need of generating normally distributed random numbers. One technique is to use the inverse cumulative normal distribution function on uniform random numbers. There are several different popular numerical implementations:

In practice, the most accurate algorithm, AS241, is of comparable speed as the newer but less accurate algorithms of MORO and ACKLAM. Acklam refinement to go to double precision (which AS241 is) kills its performance.

What about the Ziggurat on pseudo rng only? Here are the results with Mersenne-Twister-64, and using the Doornik implementation of the Ziggurat algorithm:

There is a more optimized algorithm, VIZIGNOR, also from Doornik which should be a bit faster. As expected, the accuracy is quite lower than with Sobol, and the Ziggurat looks worse. This is easily visible if one plots the implied volatilities as a function of the spot for AS241 and for ZIGNOR.

AS241 implied volatility on Mersenne-Twister

ZIGNOR implied volatility on Mersenne-Twister

Zignor is much noisier.

Note the slight bump in the scheme EULER-FT-BK that appears because the scheme, that approximates the Broadie-Kaya integrals with a trapeze (as in Andersen QE paper), does not respect martingality that well compared to the standard full truncated Euler scheme EULER-FT, and the slightly improved EULER-FT-MID where the variance integrals are approximated by a trapeze as in Van Haastrecht paper on Schobel-Zhu:

This allows to leak less correlation than the standard full truncated Euler.

In an earlier post, I mentioned the similarities between the Guyon-Labordere particle method and the Vanderstoep-Grzelak-Oosterlee “bin” method to calibrate and price under Local Stochastic volatility. I will be a bit more precise here. The same thing, really

The particle method can be seen as a generalization of the “bin” method. In deed, the bin method consists in doing the particle method using a histogram estimation of the conditional variance. The histogram estimation can be more or less seen as a very basic rectangle kernel with the appropriate bandwidth. The “bin” method is then just the particle method with another kernel (wiki link) (in the particle method, the kernel is a quartic with bandwidth defined by some slightly elaborate formula). A very good paper on this is Silverman Density estimation for statistics and data analysis, referenced by Guyon-Labordere.

In theory, the original particle method has the advantage of using a narrower bandwidth, resulting in a theoretical increase in performance as one does not have to sum over all particles, while providing a more local therefore precise estimate. In practice, the performance advantage is not so clear on my non optimized code. Two-pass There is an additional twist in the particle method: one can compute the expectation and the payoff evaluation in the same Monte-Carlo simulation, or in two sequential Monte-Carlo simulations.

Why would we do two? Mainly because the expectation is computed across all paths, at each time step, while, usually, payoff evaluation requires a full path as it will need to store some state at each observation time for path-dependent payoffs.

We can avoid recomputing the paths by just caching them at each observation time. The problem is that the size of this cache can quickly become extremely large and blow up the memory. For example a 10y daily knock-out will require 10 * 252 * 8 * 2 * MB = 40 GB for 1 million paths.

A side effect of the second simulation is that one can use a Quasi-Random number generator there, while for the first simulation, this is not easy as we compute all paths, dimension by dimension.

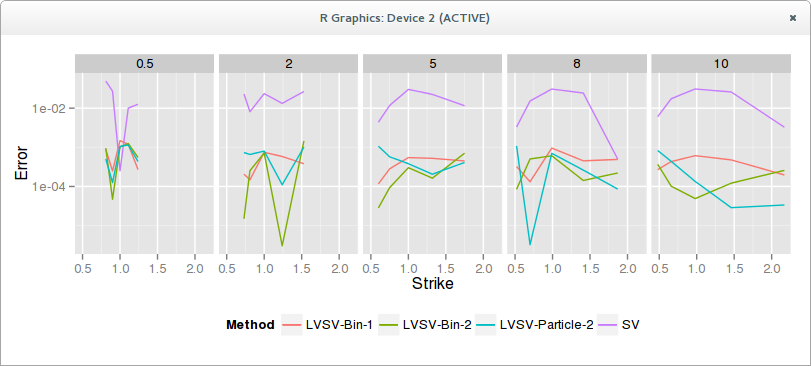

In practice, both methods work well, particle or bins, single-pass or two-pass. Here is a graph of the error in volatility, SV is a not so well calibrated Heston to market data. LVSV are the local stochastic volatility simulations, using as Vanderstoep 100 steps per year and 500K simulations with 30 bins.

The advantages of the particle do not show up in terms of accuracy on this example. I have also noticed that short expiries seem trickier, the error being larger. This might just be due to the time-step size, but interestingly the papers only show graphs of medium (min=6m) to large expiries.

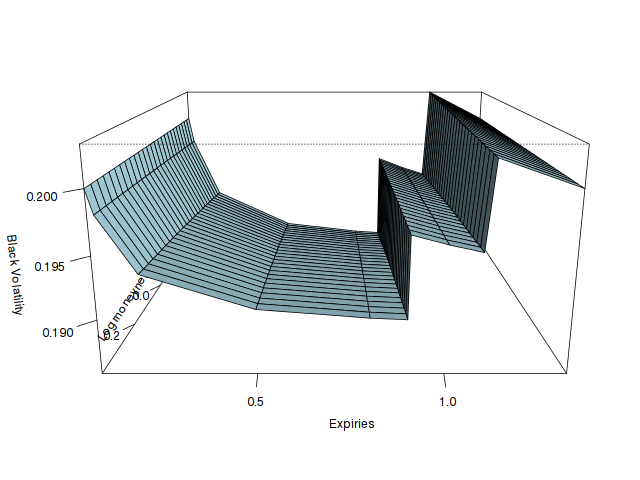

In papers around volatility and cash (discrete) dividends, we often encounter the example of the flat volatility surface. For example, the OpenGamma paper presents this graph:

It shows that if the Black volatility surface is fully flat, there are jumps in the pure volatility surface (corresponding to a process that includes discrete dividends in a consistent manner) at the dividend dates or equivalently if the pure volatility surface is flat, the Black volatility jumps.

This can be traced to the fact that the Black formula does not respect C(S,K,Td-) = C(S,K-d,Td) as the forward drops from F(Td-) to F(Td-)-d where d is dividend amount at td, the dividend ex date.

Unfortunately, those examples are not very helpful. In practice, the market observables are just Black volatility points, which can be interpolated to volatility slices for each expiry without regards to dividends, not a full volatility surface. Discrete dividends will mostly happen between two slices: the Black volatility jump will happen on some time-interpolated data.

While the jump size is known (it must obey to the call price continuity), the question of how one should interpolate that data until the jump is far from trivial even using two flat Black volatility slices.

The most logical is to consider a model that includes discrete dividends consistently. For example, one can fully lookup the Black volatility corresponding the price of an option assuming a piecewise lognormal process with jumps at the dividend dates. It can be priced by applying a finite difference method on the PDE. Alternatively, Bos & Vandermark propose a simple spot and strike adjusted Black formula that obey the continuity requirement (the Lehman model), which, in practice, stays quite close to the piecewise lognormal model price. Another possibility is to rely on a forward modelling of the dividends, as in Buehler (if one is comfortable with the idea that the option price will then depend ultimately on dividends past the option expiry).

Recently, a Wilmott article suggested to only rely on the jump adjustment, but did not really mention how to find the volatility just before or just after the dividend. Here is an illustration of how those assumptions can change the volatility in between slices using two dividends at T=0.9 and T=1.1.

In the first graph, we just interpolate linearly in forward moneyness the pure vol from the Bos & Vandermark formula, as it should be continuous with the forward (the PDE would give nearly the same result) and compute the equivalent Black volatility (and thus the jump at the dividend dates).

In the second graph, we interpolate linearly the two Black slices, until we find a dividend, at which point we impose the jump condition and repeat the process until the next slice. We process forward (while the Wilmott article processes backward) as it seemed a bit more natural to make the interpolation not depend on future dividends. Processing backward would just make the last part flat and first part down-slopping. On this example backward would be closer to the Bos Black volatility, but when the dividends are near the first slice, the opposite becomes true.

While the scale of those changes is not that large on the example considered, the choice can make quite a difference in the price of structures that depend on the volatility in between slices. A recent example I encountered is the variance swap when one includes adjustment for discrete dividends (then the prices just after the dividend date are used).

To conclude, if one wants to use the classic Black formula everywhere, the volatility must jump at the dividend dates. Interpolation in time is then not straightforward and one will need to rely on a consistent model to interpolate. It is not exactly clear then why would anyone stay with the Black formula except familiarity.

There is an interesting course on Machine Learning on Coursera, it does not require much knowledge and yet manages to teach quite a lot.

I was struck by the fact that most techniques and ideas apply also to problems in quantitative finance.

Linear regression: used for example in the Longstaff-Schwartz approach to price Bermudan options with Monte-Carlo. Interestingly the teacher insists on feature normalization, something we can forget easily, especially with the polynomial features.

Gradient descent: one of the most basic minimizer and we use minimizers all the time for model calibration.

Regularization: in finance, this is sometimes used to smooth out the volatility surface, or can be useful to add stability in calibration. The lessons are very practical, they explain well how to find the right value of the regularization parameter.

Neural networks: calibrating a model is very much like training a neural network. The backpropagation is the same thing as the adjoint differentiation. It’s very interesting to see that it is a key feature for Neural networks, otherwise training would be much too slow and Neural networks would not be practical. Once the network is trained, it is evaluated relatively quickly forward. It’s basically the same thing as calibration and then pricing.

Support vector machines: A gaussian kernel is often used to represent the frontier. We find the same idea in the particle Monte-Carlo method.

Principal component analysis: can be applied to the covariance matrix square root in Monte-Carlo simulations, or to “compress” large baskets, as well as for portfolio risk.

It’s also interesting to hear the teacher repeating that people should not try possible improvements at random (often because they have only one idea) but analyze before what makes the most sense. And that can imply digging in the details, looking at what’s going on 100 samples.

While it sounds like a straightforward remark, I have found that people (including myself) tend to do the same mistakes in finance. We might use some quadrature, find out it does not perform that well in some cases, replace it with another one that behaves a bit better, without investigating the real issue: why does the first quadrature break? is the new quadrature really fixing the issue?

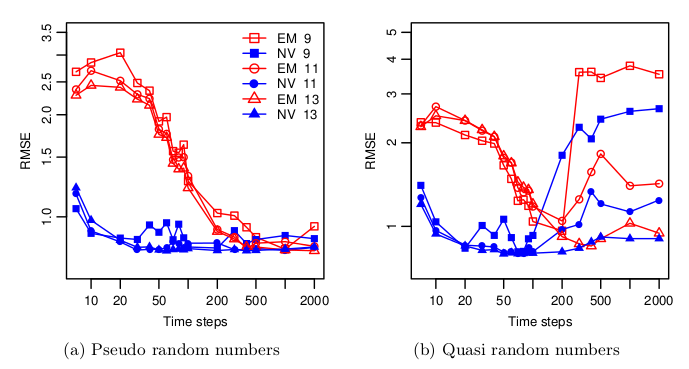

Quasi-Random numbers (like Sobol) are a relatively popular way in finance to improve the Monte-Carlo convergence compared to more classic Pseudo-Random numbers (like Mersenne-Twister). Behind the scenes one has to be a bit more careful about the dimension of the problem as the Quasi-Random numbers depends on the dimension (defined by how many random variables are independent from each other).

For a long time, Sobol was limited to 40 dimensions using the so called Bratley-Fox direction numbers (his paper actually gives the numbers for 50 dimensions). Later Lemieux gave direction numbers for up to 360 dimensions. Then, P. Jäckel proposed some extension with a random initialization of the direction vectors in his book from 2006. And finally Joe & Kuo published direction numbers for up to 21200 dimensions.

But there are very few studies about how good are real world simulations with so many quasi-random dimensions. A recent paper "Fast Ninomiya-Victoir Calibration of the Double-Mean-Reverting Model" by Bayer, Gatheral & Karlsmark tests this for once, and the results are not so pretty:

With their model, the convergence with Sobol numbers becomes worse when the number of time-steps increases, that is when the number of dimension increases. There seems to be even a threshold around 100 time steps (=300 dimensions for Euler) beyond which a much higher number of paths (2^13) is necessary to restore a proper convergence. And they use the latest and greatest Joe-Kuo direction numbers.

Still the total number of paths is not that high compared to what I am usually using (2^13 = 8192). It's an interesting aspect of their paper: the calibration with a low number of paths.

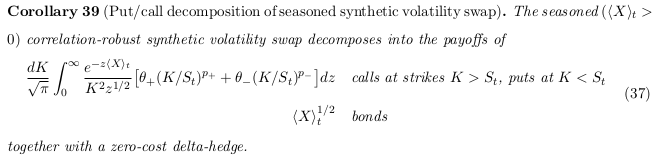

Recently, some instabilities were noticed in the Carr-Lee seasoned volatility swap price in some situations.

The Carr-Lee seasoned volatility swap price involve the computation of a double integral. The inner integral is really the problematic one as the integrand can be highly oscillating. I first found a somewhat stable behavior using a specific adaptive Gauss-Lobatto implementation (the one from Espelid) and a change of variable. But it was not very satisfying to see that the outer integral was stable only with another specific adaptive Gauss-Lobatto (the one from Gander & Gauschi, present in Quantlib). I tried various choices of adaptive (coteda, modsim, adaptsim,...) or brute force trapezoidal integration, but either they were order of magnitudes slower or unstable in some cases. Just using the same Gauss-Lobatto implementation for both would fail...

I then noticed you could write the integral as a Fourier transform as well, allowing the use of FFT. Unfortunately, while this worked, it turned out to require a very large number of points for a reasonable accuracy. This, plus the tricky part of defining the proper step size, makes the method not so practical.

I had heard before of the Filon quadrature, which I thought was more of a curiosity. The main idea is to integrate exactly x^n * cos(k*x). One then relies on a piecewise parabolic approximation of the function f to integrate f(x) * cos(k*x). Interestingly, a very similar idea has been used in the Sali quadrature method for option pricing, except one integrates exactly x^n * exp(-k*x^2).

It turned out to be remarkable on that problem, combined with a simple adaptive Simpson like method to find the right discretization. Then as if by magic, any outer integration quadrature worked.

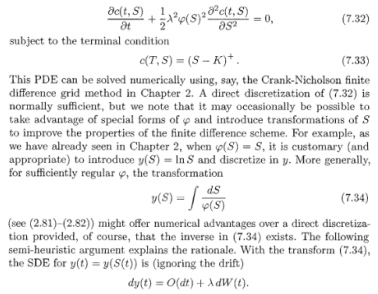

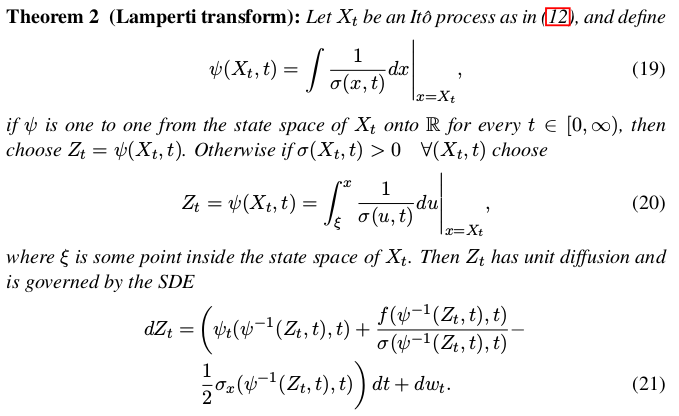

Without knowing that it was a well known general concept, I first noticed the use of the Lamperti transform in the Andersen-Piterbarg “Interest rate modeling” book p.292 “finite difference solutions for general phi”.

Today, I found a paper referencing this paper explicitly when presenting the transformation of a stochastic process to a unit diffusion in “Density estimates for solutions to one dimensional Backward SDE’s”. In addition it also references one exercise of the Karatzas-Schreve book “Brownian motion and Stochastic calculus”, which presents again the same idea, without calling it Lamperti transform.