New SABR Formulae

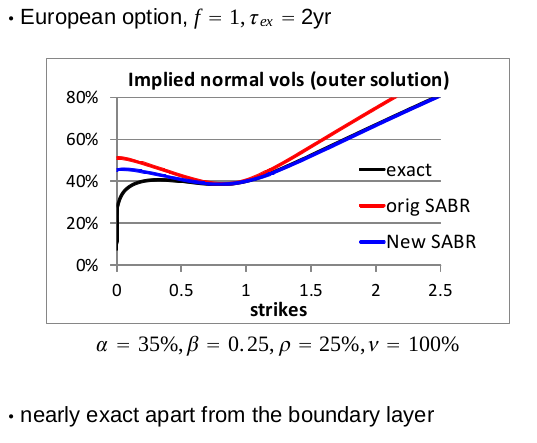

In a talk at the Global Derivatives conference of Amsterdam (2014), Pat Hagan presented some new SABR formulas, supposedly close to the arbitrage free PDE behavior.I tried to code those from the slides, but somehow that did not work out well on his example, I just had something very close to the good old SABR formulas. I am not 100% sure (only 99%) that it is due to a mistake in my code. Here is what I was looking to reproduce:

|

| Pat Hagan Global Derivatives example |

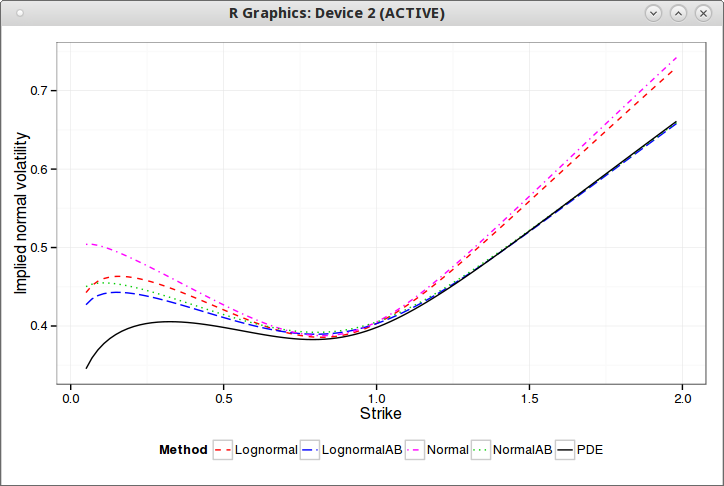

Fortunately, I then found in some thesis the idea of using Andersen & Brotherton-Ratcliffe local volatility expansion. In deed, the arbitrage free PDE from Hagan is equivalent to some Dupire local volatility forward PDE (see http://papers.ssrn.com/abstract=2402001), so Hagan just gave us the local volatility expansion to expand on (the thesis uses Doust, which is not so different in this case).

And then it produces on this global derivatives example the following:

The AB suffix are the new SABR formula. Even though the formulas are different, that looks very much like Hagan's own illustration (with a better scale)!

I have a draft paper around this and more practical ideas to calibrate SABR:

http://papers.ssrn.com/abstract=2467231