Measuring Roughness with Julia

I received a few e-mails asking me for the code I used to measure roughness in my preprint on the roughness of the implied volatility. Unfortunately, the code I wrote for this paper is not in a good state, it’s all in one long file line by line, not necessarily in order of execution, with comments that are only meaningful to myself.

In this post I will present the code relevant to measuring the oxford man institute roughness with Julia. I won’t go into generating Heston or rough volatility model implied volatilities, and focus only on the measure on roughness based on some CSV like input. I downloaded the oxfordmanrealizedvolatilityindices.csv from the Oxford Man Institute website (unfortunately now discontinued, data bought by Refinitiv but still available in some github repos) to my home directory

using DataFrames, CSV, Statistics, Plots, StatsPlots, Dates, TimeZones

df = DataFrame(CSV.File("/home/fabien/Downloads/oxfordmanrealizedvolatilityindices.csv"))

df1 = df[df.Symbol .== ".SPX",:]

dsize = trunc(Int,length(df1.close_time)/1.0)

tm = [abs((Date(ZonedDateTime(String(d),"y-m-d H:M:S+z"))-Date(ZonedDateTime(String(dfv.Column1[1]),"y-m-d H:M:S+z"))).value) for d in dfv.Column1[:]];

ivm = dfv.rv5[:]

using Roots, Statistics

function wStatA(ts, vs, K0,L,step,p)

bvs = vs # big.(vs)

bts = ts # big.(ts)

value = sum( abs(log(bvs[k+K0])-log(bvs[k]))^p / sum(abs(log(bvs[l+step])-log(bvs[l]))^p for l in k:step:k+K0-step) * abs((bts[k+K0]-bts[k])) for k=1:K0:L-K0+1)

return value

end

function meanRoughness(tm, ivm, K0, L)

cm = zeros(length(tm)-L);

for i = 1:length(cm)

local ivi = ivm[i:i+L]

local ti = tm[i:i+L]

T = abs((ti[end]-ti[1]))

try

cm[i] = 1.0 / find_zero(p -> wStatA(ti, ivi, K0, L, 1,p)-T,(1.0,100.0))

catch e

if isa(e, ArgumentError)

cm[i] = 0.0

else

throw(e)

end

end

end

meanValue = mean(filter( function(x) x > 0 end,cm))

stdValue = std(filter( function(x) x > 0 end,cm))

return meanValue, stdValue, cm

end

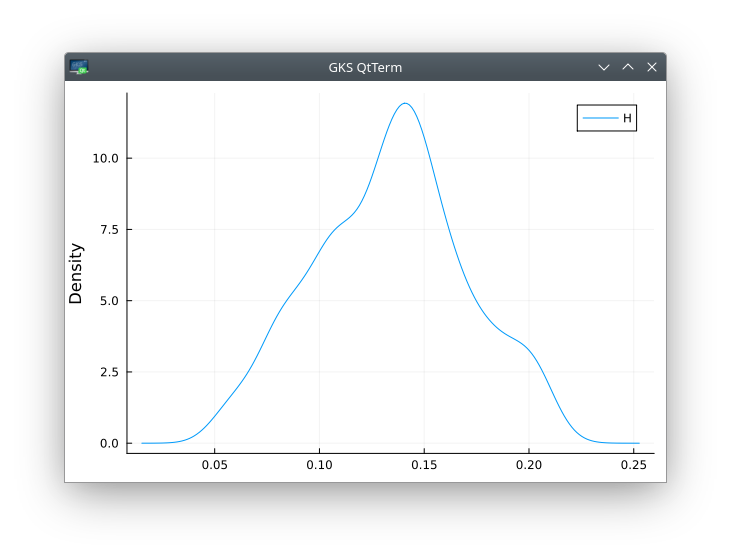

meanValue, stdValue, cm = meanRoughness(tm, ivm, K0,K0^2)

density(cm,label="H",ylabel="Density")