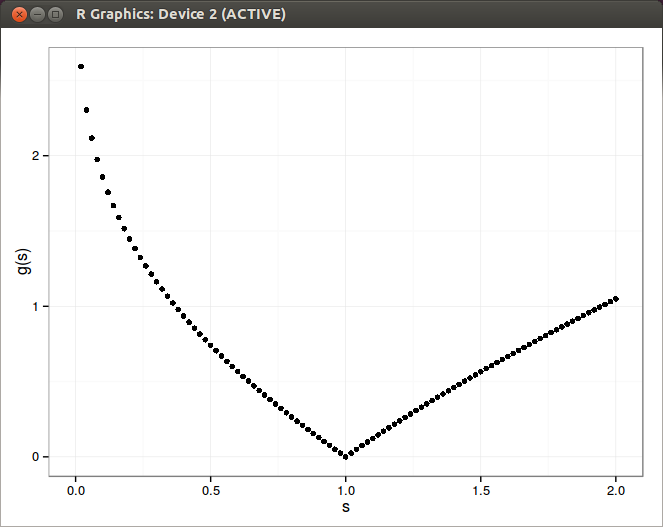

A Volatility Swap and a Straddle

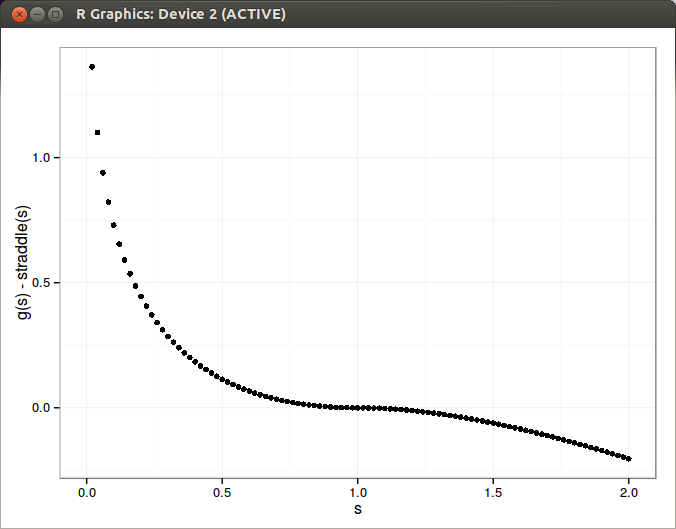

A Volatility swap is a forward contract on future realized volatility. The pricing of such a contract used to be particularly challenging, often either using an unprecise popular expansion in the variance, or a model specific way (like Heston or local volatility with Jumps). Carr and Lee have recently proposed a way to price those contracts in a model independent way in their paper “robust replication of volatility derivatives”. Here is the difference between the value of a synthetic volatility swap payoff at maturity (a newly issued one, with no accumulated variance) and a straddle.

I wonder how good is the discrete Derman approach compared to a standard integration for such a payoff as well as how important is the extrapolation of the implied volatility surface.The real payoff (very easy to obtain through Carr-Lee Bessel formula):