Integrating an oscillatory function

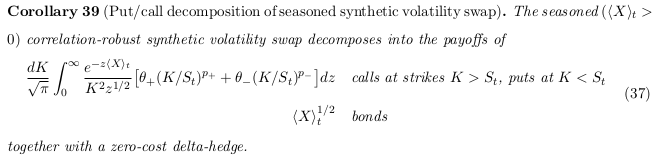

Recently, some instabilities were noticed in the Carr-Lee seasoned volatility swap price in some situations.The Carr-Lee seasoned volatility swap price involve the computation of a double integral. The inner integral is really the problematic one as the integrand can be highly oscillating.

I first found a somewhat stable behavior using a specific adaptive Gauss-Lobatto implementation (the one from Espelid) and a change of variable. But it was not very satisfying to see that the outer integral was stable only with another specific adaptive Gauss-Lobatto (the one from Gander & Gauschi, present in Quantlib). I tried various choices of adaptive (coteda, modsim, adaptsim,...) or brute force trapezoidal integration, but either they were order of magnitudes slower or unstable in some cases. Just using the same Gauss-Lobatto implementation for both would fail...

I then noticed you could write the integral as a Fourier transform as well, allowing the use of FFT. Unfortunately, while this worked, it turned out to require a very large number of points for a reasonable accuracy. This, plus the tricky part of defining the proper step size, makes the method not so practical.

I had heard before of the Filon quadrature, which I thought was more of a curiosity. The main idea is to integrate exactly x^n * cos(k*x). One then relies on a piecewise parabolic approximation of the function f to integrate f(x) * cos(k*x). Interestingly, a very similar idea has been used in the Sali quadrature method for option pricing, except one integrates exactly x^n * exp(-k*x^2).

It turned out to be remarkable on that problem, combined with a simple adaptive Simpson like method to find the right discretization. Then as if by magic, any outer integration quadrature worked.